This week: Health Savings Accounts (HSAs) were designed to pay for medical expenses with tax-free dollars, sort of like a Flexible Spending Account. But, since unused funds roll over from year to year, they can also be a great savings vehicle for account holders who make regular contributions. And, for those who do, HSAs actually offer a triple-tax advantage: the money goes in tax free (you get an immediate tax break), it grows tax free (earning interest and/or investment income), and, if it’s used for eligible medical expenses when withdrawn, it’s always tax free. This week, we explain those three benefits and show you some real numbers so you can see how big the tax savings can be.

What is an HSA?

Health Savings Accounts (HSAs) are tax-advantaged savings and investing accounts that people can open when they’re enrolled in an HSA-eligible High-Deductible Health Plan (HDHP).

In plain English, an HDHP is a health plan that meets specific IRS rules for a higher deductible and a capped annual out-of-pocket limit; outside of preventive care (which is typically covered first-dollar), you generally pay the cost of care until the deductible is met.

HSAs pair with these plans to let you set money aside, often through payroll, to pay for current and future medical expenses more efficiently.

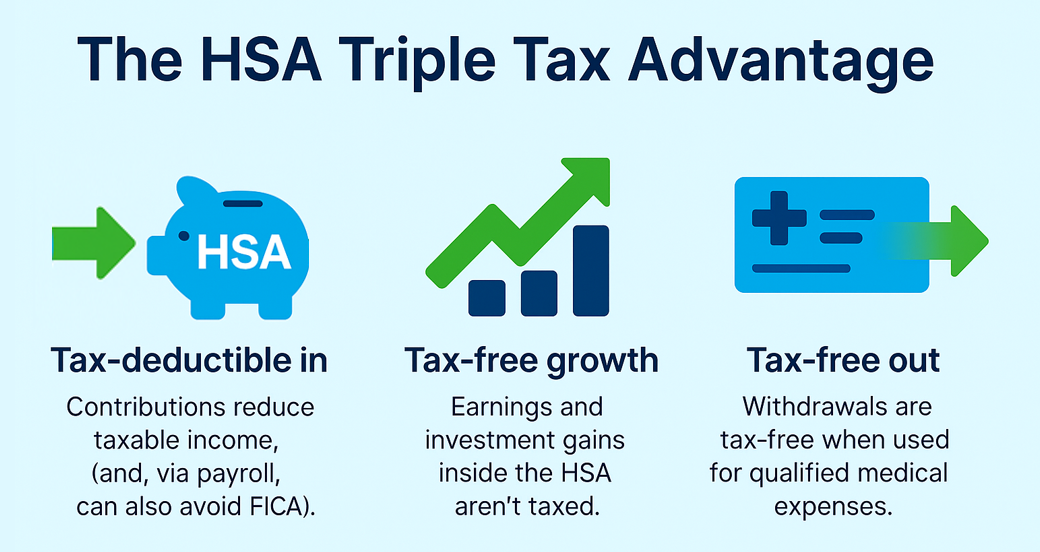

Triple Tax Benefit

The appeal is simple: HSAs offer a powerful, three-part tax benefit.

Yet many people, employees and individual consumers, employers choosing plan designs, and even brokers, struggle to explain how those three pieces work together or to quantify the real-world savings. This article fixes that by walking through clear examples with actual numbers so you can see just how significant the advantages can be.

In the sections that follow, we’ll use simple examples, centered on a single filer earning around $60,000, to compare HSAs with other common accounts and show the savings step by step. (Higher earners are typically in higher brackets and often save even more.)

Federal Tax Savings

Federal Income Tax

The amount that HSA account holders can save depends on their federal income tax rate, which of course is determined by their income. Below are the federal tax brackets for 2026.

| Rate | Single | Married Filing Jointly |

|---|---|---|

| 10% | $0, $11,925 | $0, $23,850 |

| 12% | $11,925, $48,475 | $23,850, $96,950 |

| 22% | $48,475, $103,350 | $96,950, $206,700 |

| 24% | $103,350, $197,300 | $206,700, $394,600 |

| 32% | $197,300, $250,525 | $394,600, $501,050 |

| 35% | $250,525, $626,350 | $501,050, $751,600 |

| 37% | $626,350 and up | $751,600 and up |

FICA Savings

Save on FICA too!

When employees contribute to an HSA through payroll under a Section 125 cafeteria plan, those dollars usually avoid both federal income tax and FICA (Social Security + Medicare) of 7.65%.

For someone earning about $60,000, typically in the 22% federal bracket, that’s roughly 22% + 7.65% ≈ 29.65% in avoided taxes on HSA dollars (nearly a 30% “instant discount” on qualified medical costs). If your state has an income tax and treats HSA contributions as pre-tax, add that rate too for even greater savings; state rules vary.

Tax Benefit #1: Deposits

Tax Benefit #1: DEPOSITS. Immediate Savings You Can Feel

Not everyone approaches a Health Savings Account (HSA) the same way, and that’s perfectly fine. In fact, there are two common strategies, each with its own benefits:

1. The “Max-It-Out” Approach

Some people treat their HSA like a long-term savings and investment vehicle. They contribute up to the annual limit, take the instant tax deduction, and let their account grow year after year. In 2025, for example, the single contribution limit (under age 55) is $4,300. Contributing through payroll avoids both federal income tax and FICA tax: almost a 30% savings for many people, or about $1,275 in tax savings this year. Even if you contribute outside of payroll, you’ll still capture the income tax deduction, about $946 saved at a 22% bracket.

2. The “Pay-As-You-Go” Approach

Others may not be in a position to max out their contributions, but that doesn’t mean they can’t benefit. Chances are, you’re going to have medical expenses anyway. Instead of paying those bills with after-tax dollars, you can first deposit the expense amount into your HSA and then pay the provider from the account. Doing so gives you an immediate tax break on money you were going to spend regardless.

Think of it as getting a “discount” equal to your federal tax rate, or your federal rate plus 7.65% FICA if you contribute through payroll. For example, a $1,000 medical bill might really cost you only $703.50 out of pocket if funded through payroll (about a 29.65% savings), or $780 if you contribute outside payroll and only avoid federal income tax.

Use the calculator below to see how much you can save with your own numbers. It’s a simple way to understand what you’re really paying for care in after-tax dollars when you route payments through your HSA.

Tax Benefit #2: Growth

Tax Benefit #2: GROWTH. Let Compounding Work (Tax-Free!)

When someone contributes regularly to a Health Savings Account, it can really add up. Remember, the account holder gets an instant deduction on any amount deposited (similar to a 401k or an IRA), the funds in the account grow tax free, earning interest and/or investment income, and as long as the money is withdrawn to pay for eligible medical, dental, or vision expenses, it’s never taxed. That’s different from an IRA or a 401k, which grow tax deferred; the account holder must pay taxes when the funds are withdrawn. And if someone has a Roth IRA, they’re not getting the instant tax savings. Instead, they have to pay taxes up-front, which reduces the investment amount.

Perhaps an example will help. Assume someone contributes $3,000 per year to an HSA, an IRA/401k, or a Roth.

Equal pre-tax cost comparison (20 years, 5% annual return). Commit the same pre-tax effort across accounts, $3,000/yr for 20 years:

| Account | $3,000/yr (20 yrs) | Taxes | Estimated after-tax value |

|---|---|---|---|

| HSA (medical use) | ≈ $99,200 | Tax-free in retirement | ≈ $99,200 |

| Traditional 401(k)/IRA | ≈ $99,200 | Taxed at withdrawal (22%) | ≈ $77,400 |

| Roth IRA | $2,340/yr contributed (after 22% tax) | Tax-free at withdrawal | ≈ $77,400 |

| Taxable account | Invest ≈ $2,110/yr | Annual tax drag | ≈ $64,500 |

For dollars earmarked for healthcare, the HSA’s combo of deductible in + tax-free growth is hard to beat, and you still haven’t seen the best part.

Tax Benefit #3: Withdrawals

Tax Benefit #3: WITHDRAWALS. The Clincher, Tax-Free Out

When you spend HSA funds on qualified medical expenses, withdrawals are tax-free. That’s what elevates HSAs beyond “tax-deferred.”

Retirement bill example: Need $2,000 at age 65 for qualified care? With an HSA, you just need to withdraw the $2,000. But with a traditional IRA or 401k, you need to withdraw the $2,000 to cover the medical bill plus the applicable taxes – in our example, an additional 22%, or $564. With a Roth IRA, the withdrawal is tax-free, but remember that the contributions were made with after-tax dollars, not pre-tax like with an HSA.

How to Explain This

How to Explain It in 10 Seconds

“If you’ll spend money on healthcare anyway, the HSA lets you pay with pre-tax dollars, grow the leftovers tax-free, and later spend them tax-free again. Most accounts only give you one or two of those.”

Some Important Notes

- Payroll vs. personal HSA funding: Payroll typically avoids both income tax and FICA; personal contributions usually avoid income tax only.

- Keep receipts: You can reimburse later for qualified expenses incurred after the HSA was opened.

- Invest the excess: Keep a small cash buffer for near-term expenses, then invest the rest in low-cost funds if your HSA allows it.

- Medicare timing: New HSA contributions generally stop once you enroll in Part A, plan ahead before filing.

- Last-month rule: If you use the Dec 1 rule to contribute the full year, you must stay HSA-eligible through the following year (testing period) or face income inclusion and a penalty.

- Non-qualified spending: Taxes (and possibly a penalty) apply, know what’s eligible.

Final Thoughts

Health Savings Accounts stand out because they offer something rare in the tax world: a triple advantage. Contributions lower your taxable income right away, balances can grow through interest or investments without annual tax drag, and qualified withdrawals are tax-free. That combination means HSAs can serve two very different purposes equally well.

Some people will use their HSA like a checking account for ongoing medical expenses, enjoying what feels like a built-in discount on the care they’re already paying for. Others will treat it as a long-term savings vehicle, letting contributions accumulate over time to cover future healthcare costs in retirement. Both strategies are valid, and the right approach often depends on cash flow, health needs, and personal goals.

The key takeaway is that you don’t have to choose one or the other on day one. HSAs are flexible enough to adjust as your situation changes, making them one of the most versatile benefits available to people with high-deductible health plans.