This week: Reference-based pricing is often discussed as if it’s one specific type of plan, but that’s not the case. This article breaks down the different ways RBP is structured, the tradeoffs involved, and what advisors need to clarify before making a recommendation.

Reference-based pricing is one of those terms that gets thrown around a lot in the benefits world, but not always in a consistent way.

Depending on who you talk to, it can mean anything from a disruptive, no-network plan to a more structured model that still uses provider networks in certain situations. That’s part of the problem, people think they’re talking about the same thing when they’re not.

At a high level, the concept is straightforward. Instead of relying entirely on carrier-negotiated networks, a reference-based pricing plan uses a benchmark, often a percentage of Medicare, to determine what it will pay for services. As the International Foundation of Employee Benefit Plans explains, employer-sponsored RBP arrangements typically reimburse providers based on a defined percentage above Medicare rates rather than traditional network discounts.

That sounds simple enough, but in practice, there are several different ways to structure a plan around that idea. And those differences matter.

Why Employers Are Even Looking at This

Before getting into the different models, it’s worth stepping back and asking why this is even a conversation.

Health plan costs continue to rise year after year, and employers are feeling that pressure. According to KFF, the average annual premium for family coverage has climbed to nearly $27,000, which makes it increasingly difficult for employers to maintain traditional plan designs without significant cost increases.

That environment is what’s driving interest in alternatives. Reference-based pricing is one of those alternatives, but it’s not a single, uniform solution.

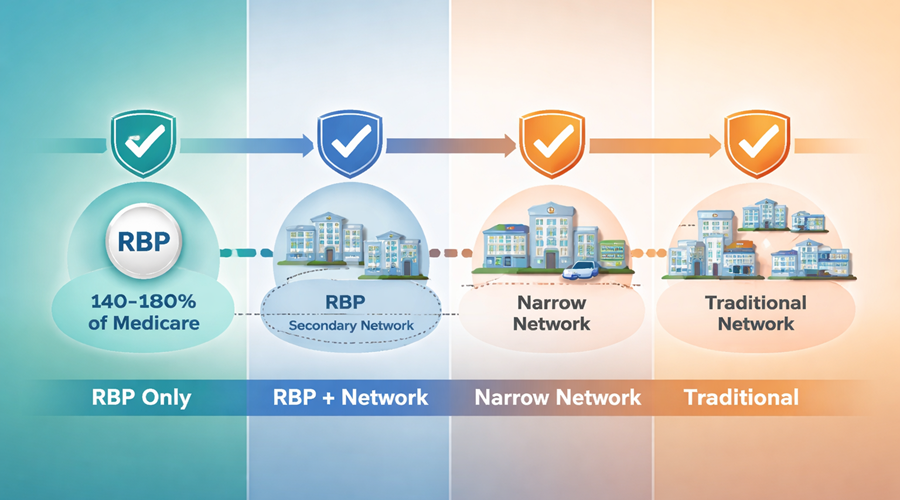

Reference-Based Pricing Is Not One Thing

One of the biggest misconceptions is that reference-based pricing is a specific type of plan. In reality, it’s better thought of as a strategy that can be implemented in different ways.

At one end of the spectrum, you have what most people think of as “pure” RBP. These plans do not rely on a traditional PPO network. Instead, they pay a set percentage of Medicare, for example, 140% to 180%, and use advocacy and negotiation services to work directly with providers.

This approach can create significant savings, but it also introduces more disruption. Providers may not accept the payment, and there is a greater need for employee education and support.

From there, you move into hybrid models. Some plans still use a Medicare-based benchmark as the foundation but layer in additional tools, such as secondary networks or negotiated arrangements, to reduce friction when providers are unwilling to accept the reference price.

And then there are models that don’t technically fall under RBP but are trying to solve a similar problem. Narrow networks, high-performance networks, and steerage-based designs all aim to control costs by guiding employees toward more efficient providers. As the Commonwealth Fund notes, these types of strategies can lower spending but may also limit provider choice or create tradeoffs for employees.

The point is that when someone says “we’re looking at reference-based pricing,” that statement alone doesn’t tell you enough. You have to understand which version they’re actually considering.

The Tradeoffs Are Different for Each Model

Because these models vary, the tradeoffs vary as well.

More aggressive approaches tend to offer greater potential savings, but they also require more change. That can mean adjusting employee expectations, handling provider negotiations differently, and putting stronger support systems in place.

More structured or hybrid approaches may feel more familiar and reduce disruption, but they often come with higher costs relative to pure RBP.

That’s why this isn’t a question of whether reference-based pricing “works.” It’s a question of which version aligns with the employer’s goals, risk tolerance, and workforce.

Where Advisors Add Value

This is where the role of the advisor becomes critical.

Employers don’t just need a recommendation. They need clarity. They need to understand what they’re actually buying, how it works, and what to expect once it’s implemented.

That starts with asking better questions:

- Is this a pure RBP model or a hybrid approach?

- What happens when a provider does not accept the reference price?

- What support is in place for employees?

- How much disruption should we expect?

Those questions lead to better decisions, and better decisions lead to better outcomes.

The Bigger Picture

Reference-based pricing is not a silver bullet, and it’s not the right fit for every group.

But it is part of a broader shift in how employers think about managing healthcare costs. Instead of accepting whatever increases come their way, more employers are exploring alternatives and asking how their plans are structured in the first place.

That’s a good thing.

Because once that conversation starts, it usually leads to better questions, better strategies, and ultimately, better decisions.